Strategic Financial Planning and Wealth Management

Diamond Partners|Sunshine Coast

Long-term advice built on trust and experience

At Diamond Partners, we understand that wealth management is about more than managing finances, it’s about creating a secure future with your personal goals and lifestyle in mind. Since 2014, we have partnered with business owners, established investors and pre-retirees seeking strategic financial planning, succession planning and long-term wealth management advice.

Our team brings over 92 years of combined financial planning experience, providing clients with trusted advice, investment oversight and tailored financial strategies designed to support long-term objectives. Whether you’re building wealth, preparing for retirement or reviewing an existing strategy, we bring a coordinated and personalised approach to financial advice.

We are committed to helping clients simplify complex financial decisions with clarity and confidence. Through strategic financial planning, investment management and ongoing guidance, we help clients focus on what matters most. Their family, lifestyle and long-term financial future.

At Diamond Partners, we bring confidence to complexity and clarity to strategy. Supported by deep experience, senior acumen and considered advice.

Our Services

Experience the ‘Diamond Difference’ by adding our team to yours.

Tailored and personalised financial planning for high-net-worth individuals, families, and successful business owners.

Strategic Investment Advice

Tailored investment strategies and portfolio oversight focused on long-term growth, diversification and wealth preservation.

Succession and Tax

Succession planning and tax-effective strategies designed to support wealth preservation and long-term financial outcomes.

Holistic Wealth Management

Coordinated wealth management designed to align investment, retirement and financial strategies with long-term objectives.

Continued Care

Ongoing advice and annual strategy reviews designed to keep your financial plan aligned with evolving goals and changing circumstances.

Retirement Planning

Retirement planning strategies designed to support long-term financial confidence, sustainable income and lifestyle objectives.

Financial Advice

Strategic financial advice to help clients navigate wealth management, retirement planning and long-term financial decisions with confidence.

Financial Insights and Resources

Explore our blog posts and market insights designed to help you make informed financial decisions and build long-term financial security.

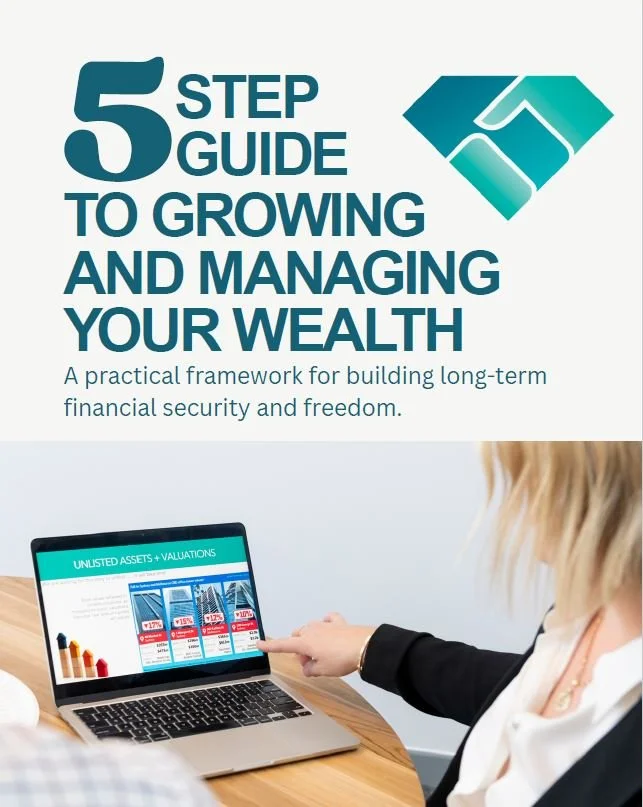

Download Your Free 5-Step Guide to Growing and Managing Your Wealth.

A practical framework designed to help you build wealth, make informed financial decisions, and create long-term financial security.

Our website contents provide general information only and does not constitute financial or tax advice. Tax outcomes depend on individual circumstances and current legislation. Always seek personalised advice from a qualified professional before implementing any financial strategies.

Inside the Guide

✓ Understand Your Money

✓ Your Financial Foundation

✓ Long Term Mindset

✓ Structure Your Wealth

✓ Create Financial Freedom and Legacy